3 ASX Growth Stocks With Insider Ownership And Up To 32% ROE

The Australian market has shown positive momentum, climbing 1.1% in the last week and achieving a 17% increase over the past year, with earnings projected to grow by 12% annually. In this environment, stocks that combine strong growth potential with significant insider ownership can be particularly attractive, as they often indicate confidence from those closest to the company's operations.

Top 10 Growth Companies With High Insider Ownership In Australia

Name | Insider Ownership | Earnings Growth |

Clinuvel Pharmaceuticals (ASX:CUV) | 10.4% | 27.4% |

Genmin (ASX:GEN) | 12% | 117.7% |

Catalyst Metals (ASX:CYL) | 14.8% | 45.4% |

AVA Risk Group (ASX:AVA) | 15.7% | 118.8% |

Liontown Resources (ASX:LTR) | 14.7% | 59.8% |

Hillgrove Resources (ASX:HGO) | 10.4% | 70.2% |

Acrux (ASX:ACR) | 17.4% | 91.6% |

Pointerra (ASX:3DP) | 20.1% | 126.4% |

Adveritas (ASX:AV1) | 21.2% | 144.2% |

Plenti Group (ASX:PLT) | 12.8% | 106.4% |

Let's dive into some prime choices out of the screener.

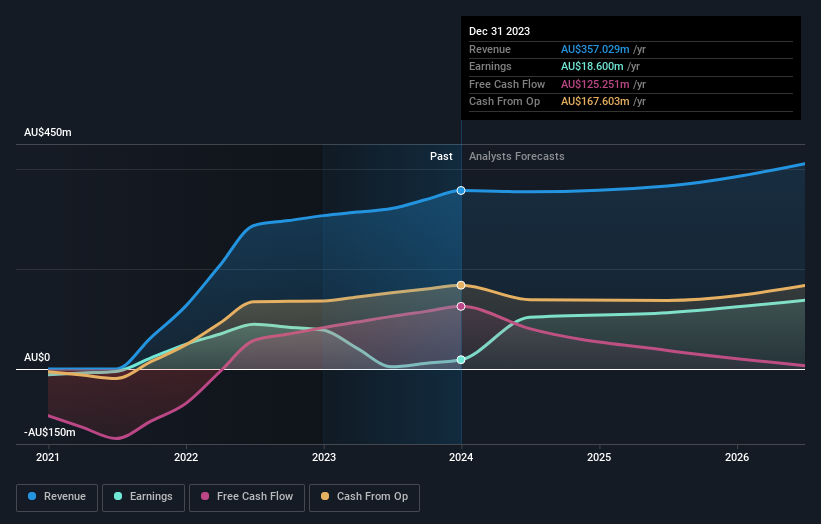

Capricorn Metals

Simply Wall St Growth Rating: ★★★★★☆

Overview: Capricorn Metals Ltd is an Australian company focused on the evaluation, exploration, development, and production of gold properties, with a market cap of A$2.43 billion.

Operations: The company's revenue is primarily generated from its Karlawinda gold operation, amounting to A$359.73 million.

Insider Ownership: 11.9%

Return On Equity Forecast: 33% (2027 estimate)

Capricorn Metals exhibits significant growth potential, with earnings forecasted to grow at 20.5% annually, outpacing the Australian market. Recent financials show a substantial increase in net income to A$87.14 million from A$4.4 million year-on-year, reflecting robust operational performance. The Karlawinda Gold Project expansion study aims to boost throughput by up to 55%, potentially enhancing production capacity and resource conversion rates—factors that could further drive growth and value creation for stakeholders.

Cettire

Simply Wall St Growth Rating: ★★★★★☆

Overview: Cettire Limited operates as an online luxury goods retailer in Australia, the United States, and internationally, with a market cap of A$850.16 million.

Operations: The company generates revenue through online retail sales amounting to A$742.26 million.

Insider Ownership: 33.5%

Return On Equity Forecast: 33% (2027 estimate)

Cettire demonstrates strong growth prospects, with earnings expected to increase significantly at 29% annually, surpassing the Australian market. Despite a volatile share price recently, insider confidence is evident through substantial buying activity. Revenue for fiscal 2024 was A$742.26 million, up from A$416.23 million last year; however, net income decreased to A$10.47 million from A$15.97 million due to narrower profit margins. The recent appointment of Caroline Elliott as a Non-Executive Director may bolster strategic oversight and governance.

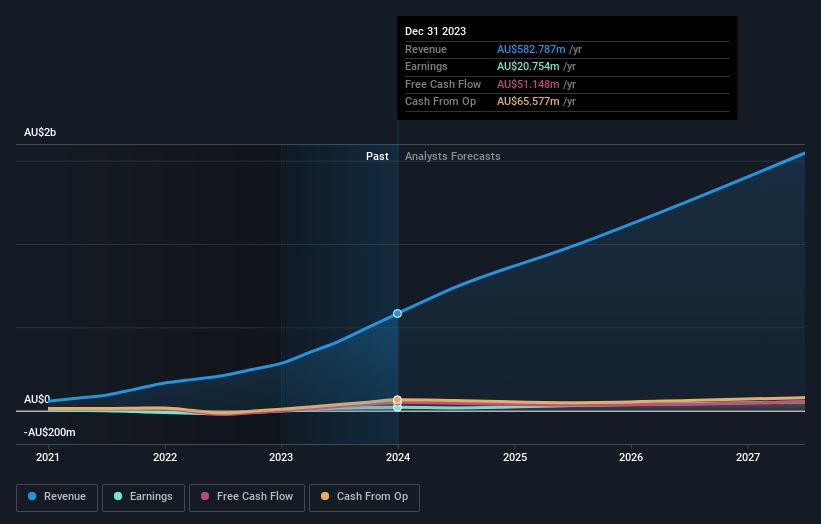

Emerald Resources

Simply Wall St Growth Rating: ★★★★★★

Overview: Emerald Resources NL is involved in the exploration and development of mineral reserves in Cambodia and Australia, with a market cap of A$2.73 billion.

Operations: The company's revenue primarily comes from its mine operations, generating A$366.04 million.

Insider Ownership: 18%

Return On Equity Forecast: 23% (2027 estimate)

Emerald Resources shows promising growth potential with earnings expected to grow 32.2% annually, outpacing the Australian market. Revenue is also forecasted to increase by 31.1% per year. Despite past shareholder dilution, the company trades at a significant discount to its estimated fair value. Recent results highlighted sales of A$371.07 million and net income of A$84.27 million for fiscal 2024, while Simon Lee AO's impending retirement may impact leadership dynamics moving forward.

Next Steps

Take a closer look at our Fast Growing ASX Companies With High Insider Ownership list of 97 companies by clicking here.

Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready For A Different Approach?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include ASX:CMM ASX:CTT and ASX:EMR.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]