Exploring Undervalued Swedish Stocks On The Exchange With Discounts Ranging From 18% To 27.7%

As global markets exhibit mixed signals with some regions showing economic cooling and others grappling with inflation pressures, the Swedish stock market presents unique opportunities for investors seeking value. Amidst these varied conditions, identifying undervalued stocks becomes crucial as they may offer potential for growth when the broader market conditions stabilize.

Top 10 Undervalued Stocks Based On Cash Flows In Sweden

Name | Current Price | Fair Value (Est) | Discount (Est) |

RVRC Holding (OM:RVRC) | SEK45.50 | SEK87.58 | 48% |

Nordic Waterproofing Holding (OM:NWG) | SEK161.60 | SEK308.34 | 47.6% |

Lindab International (OM:LIAB) | SEK227.20 | SEK425.81 | 46.6% |

Stille (OM:STIL) | SEK205.00 | SEK395.12 | 48.1% |

Biotage (OM:BIOT) | SEK167.60 | SEK318.87 | 47.4% |

Flexion Mobile (OM:FLEXM) | SEK8.02 | SEK15.96 | 49.7% |

Hexatronic Group (OM:HTRO) | SEK54.50 | SEK106.22 | 48.7% |

Sinch (OM:SINCH) | SEK23.70 | SEK43.73 | 45.8% |

Nordisk Bergteknik (OM:NORB B) | SEK17.10 | SEK32.19 | 46.9% |

Image Systems (OM:IS) | SEK1.495 | SEK2.85 | 47.6% |

Let's explore several standout options from the results in the screener

Vitrolife

Overview: Vitrolife AB (publ) specializes in providing assisted reproduction products and has a market capitalization of approximately SEK 22.87 billion.

Operations: The company's revenue is primarily generated from three segments: Consumables (SEK 1.56 billion), Technologies (SEK 649 million), and Genetic Services (SEK 1.29 billion).

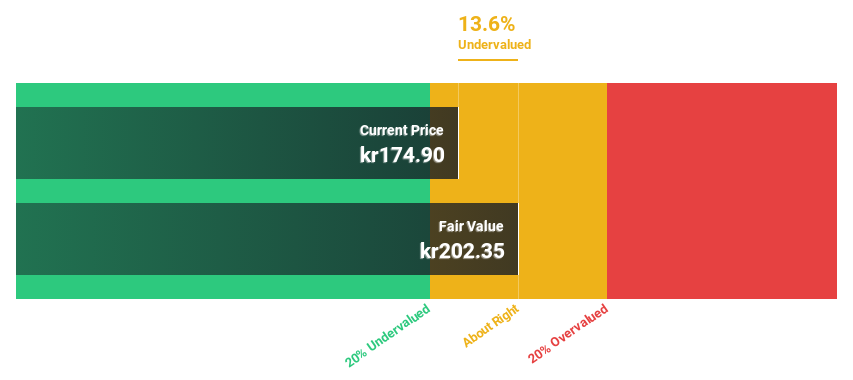

Estimated Discount To Fair Value: 18.1%

Vitrolife, currently priced at SEK168.9, is trading below its estimated fair value of SEK206.22, reflecting an 18.1% undervaluation based on discounted cash flows. Recent financial performance shows robust growth with a net income increase from SEK 100 million to SEK 115 million in Q1 2024, and earnings per share rising from SEK 0.74 to SEK 0.85. Despite this positive trajectory and a dividend increase to SEK 1.00 per share, revenue growth forecasts at 6.9% annually are modest compared to the market's expectations of faster expansions but still outpace the broader Swedish market's forecasted growth of 1.8%. Analysts anticipate the stock price could rise by approximately 37%, aligning with Vitrolife’s potential for profitability within three years amidst an average market growth context.

Xvivo Perfusion

Overview: Xvivo Perfusion AB, a medical technology company based in Sweden, specializes in developing and marketing machines and solutions for organ assessment and preservation before transplantation, operating globally with a market capitalization of SEK 13.14 billion.

Operations: The company generates revenue primarily through three segments: Services (SEK 81.13 million), Thoracic (SEK 414.34 million), and Abdominal (SEK 147.49 million).

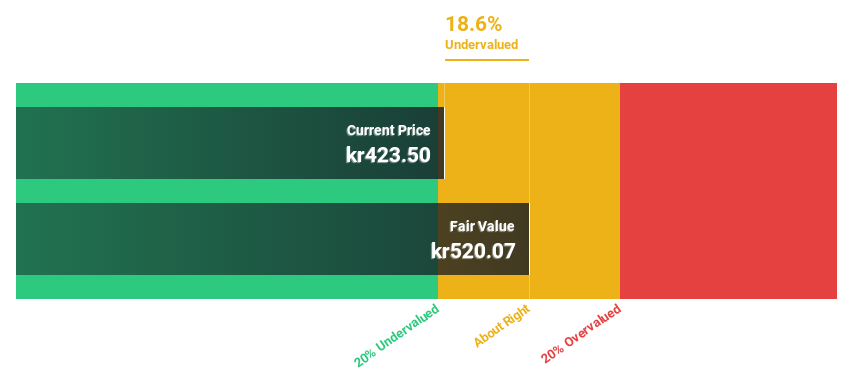

Estimated Discount To Fair Value: 27.7%

Xvivo Perfusion, with a recent share price of SEK417, appears undervalued by over 20%, as its fair value is estimated at SEK576.4 based on discounted cash flows. The company's financial health is robust, evidenced by a significant increase in sales to SEK 186.02 million and net income to SEK 22.79 million in Q1 2024. Additionally, XVIVO's revenue and earnings are expected to grow at an annual rate of 27.5% and 36.3%, respectively, outpacing the Swedish market significantly. However, concerns include shareholder dilution over the past year and a forecasted low return on equity of only 8.6% in three years.

Yubico

Overview: Yubico AB specializes in authentication solutions for computers, networks, and online services, with a market capitalization of SEK 20.84 billion.

Operations: The company generates SEK 1.93 billion from its Security Software & Services segment.

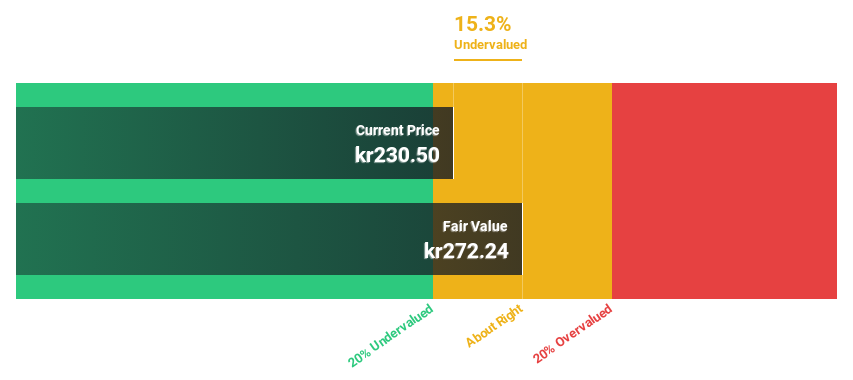

Estimated Discount To Fair Value: 18%

Yubico AB, trading at SEK242, is currently below its estimated fair value of SEK295.25, indicating potential undervaluation based on discounted cash flow analysis. The company's revenue has grown by 19.9% over the past year and is expected to increase at a rate of 22.9% annually, outpacing the Swedish market significantly. Despite this growth, Yubico faces challenges such as substantial shareholder dilution and a decrease in profit margins from 16.9% to 8.6%. Recent product updates and leadership changes signal ongoing strategic shifts aimed at enhancing security solutions for enterprises.

The analysis detailed in our Yubico growth report hints at robust future financial performance.

Dive into the specifics of Yubico here with our thorough financial health report.

Key Takeaways

Navigate through the entire inventory of 44 Undervalued Swedish Stocks Based On Cash Flows here.

Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Looking For Alternative Opportunities?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include OM:VITR OM:XVIVO and OM:YUBICO.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]