3 ASX Dividend Stocks To Consider With Yields Up To 6.3%

The Australian market has remained flat over the last week, but it has shown an impressive 18% rise over the past 12 months with earnings projected to grow by 12% annually. In this environment, dividend stocks can be appealing as they offer potential income alongside capital appreciation, making them a worthwhile consideration for investors seeking stability and growth.

Top 10 Dividend Stocks In Australia

Name | Dividend Yield | Dividend Rating |

Perenti (ASX:PRN) | 7.88% | ★★★★★☆ |

Super Retail Group (ASX:SUL) | 6.58% | ★★★★★☆ |

Nick Scali (ASX:NCK) | 4.12% | ★★★★★☆ |

Collins Foods (ASX:CKF) | 3.27% | ★★★★★☆ |

Fiducian Group (ASX:FID) | 4.65% | ★★★★★☆ |

MFF Capital Investments (ASX:MFF) | 3.66% | ★★★★★☆ |

National Storage REIT (ASX:NSR) | 4.49% | ★★★★★☆ |

Premier Investments (ASX:PMV) | 4.51% | ★★★★★☆ |

Sugar Terminals (NSX:SUG) | 7.81% | ★★★★☆☆ |

Australian United Investment (ASX:AUI) | 3.32% | ★★★★☆☆ |

Click here to see the full list of 39 stocks from our Top ASX Dividend Stocks screener.

Let's dive into some prime choices out of the screener.

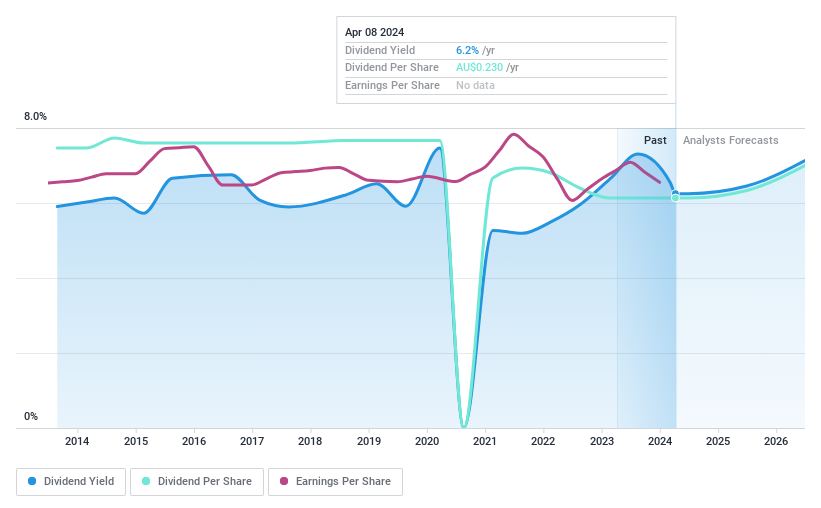

MyState

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: MyState Limited, with a market cap of A$402.72 million, operates in Australia offering banking, trustee, and managed fund products and services through its subsidiaries.

Operations: MyState Limited generates revenue through its segments, with A$135.47 million from Banking and A$15.68 million from Wealth Management.

Dividend Yield: 6.3%

MyState's dividend yield of 6.34% places it among the top 25% of Australian dividend payers, but its track record has been volatile and unreliable over the past decade. The payout ratio stands at a reasonable 71.8%, suggesting dividends are currently covered by earnings, with forecasts indicating continued coverage in three years at a similar level. However, MyState's allowance for bad loans is low at 10%, which could pose risks to future stability.

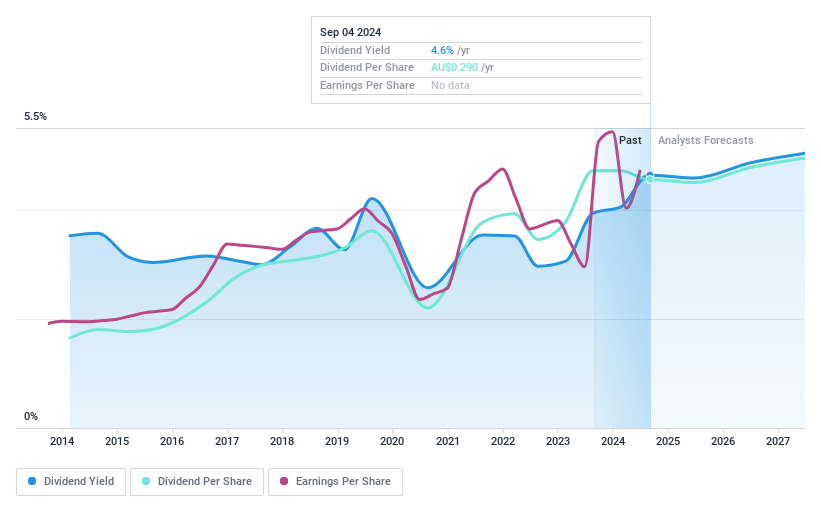

nib holdings

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: nib holdings limited, along with its subsidiaries, operates in the underwriting and distribution of private health, life, and living insurance for residents, international students, and visitors in Australia and New Zealand with a market cap of A$2.91 billion.

Operations: nib holdings limited generates revenue through several segments, including Australian Residents Health Insurance (A$2.65 billion), New Zealand Insurance (A$373.10 million), International (Inbound) Health Insurance (A$203.50 million), NIB Travel (A$96.80 million), and Nib Thrive (A$51.30 million).

Dividend Yield: 4.8%

nib holdings' dividend yield of 4.83% is below the top 25% of Australian dividend payers, and its track record has been volatile over the past decade. Despite this, dividends are covered by earnings with a payout ratio of 75.3%, and cash flows support sustainability with a cash payout ratio of 67.4%. Recent earnings growth to A$185.6 million enhances coverage prospects, though significant insider selling may signal caution for future stability.

Servcorp

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Servcorp Limited offers executive serviced and virtual offices, coworking spaces, along with IT, communications, and secretarial services, with a market cap of A$530.82 million.

Operations: Servcorp Limited generates revenue from its Real Estate - Rental segment, amounting to A$314.89 million.

Dividend Yield: 4.4%

Servcorp's dividend yield of 4.39% is lower than the top 25% of Australian dividend payers, and its history has been unreliable. However, dividends are well-covered by earnings with a payout ratio of 59.7%, and cash flows with a cash payout ratio of 14.2%. Recent earnings growth to A$39.04 million supports sustainability, alongside a declared final dividend increase to 13 cents per share for fiscal year 2024, indicating potential stability in payouts moving forward.

Next Steps

Navigate through the entire inventory of 39 Top ASX Dividend Stocks here.

Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready For A Different Approach?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include ASX:MYS ASX:NHF and ASX:SRV.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]