3 ASX Stocks Estimated To Be Trading At Discounts Of 20.8% To 37.8%

The market has climbed 2.5% in the last 7 days, with a gain of 4.5%, and over the past 12 months, it is up 11%. Earnings are forecast to grow by 13% annually, making it an opportune time to identify stocks trading below their intrinsic value. In this article, we will explore three ASX stocks currently estimated to be trading at discounts ranging from 20.8% to 37.8%, presenting potential opportunities for investors looking to capitalize on undervalued assets in a growing market.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

Name | Current Price | Fair Value (Est) | Discount (Est) |

LaserBond (ASX:LBL) | A$0.71 | A$1.37 | 48.1% |

Elders (ASX:ELD) | A$9.33 | A$18.11 | 48.5% |

Regal Partners (ASX:RPL) | A$3.40 | A$6.63 | 48.7% |

Shine Justice (ASX:SHJ) | A$0.72 | A$1.35 | 46.7% |

Megaport (ASX:MP1) | A$11.21 | A$21.52 | 47.9% |

Domino's Pizza Enterprises (ASX:DMP) | A$33.76 | A$63.86 | 47.1% |

hipages Group Holdings (ASX:HPG) | A$1.16 | A$2.31 | 49.7% |

Treasury Wine Estates (ASX:TWE) | A$12.23 | A$24.19 | 49.4% |

Millennium Services Group (ASX:MIL) | A$1.145 | A$2.24 | 48.9% |

Airtasker (ASX:ART) | A$0.27 | A$0.52 | 48.4% |

Let's take a closer look at a couple of our picks from the screened companies.

Life360

Overview: Life360, Inc. operates a technology platform for locating people, pets, and things across North America, Europe, the Middle East, Africa, and internationally with a market cap of A$4.03 billion.

Operations: The company's revenue primarily comes from its Software & Programming segment, which generated $328.68 million.

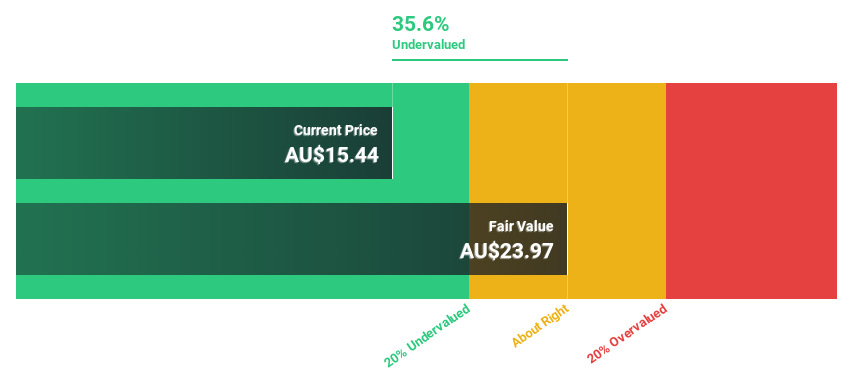

Estimated Discount To Fair Value: 37.8%

Life360 is trading at A$18.12, significantly below its estimated fair value of A$29.15, indicating it may be undervalued based on cash flows. Despite recent shareholder dilution and substantial insider selling, the company’s revenue is forecast to grow 15.7% per year, outpacing the Australian market's 5.3%. Recent partnerships with Arity and Placer.ai are expected to generate incremental revenue in 2024 and beyond, supporting Life360's pursuit of profitability within three years.

Insights from our recent growth report point to a promising forecast for Life360's business outlook.

Unlock comprehensive insights into our analysis of Life360 stock in this financial health report.

IPD Group

Overview: IPD Group Limited, with a market cap of A$474.51 million, distributes electrical equipment in Australia.

Operations: The company generates revenue from two main segments: A$215.98 million from its Products Division and A$20.79 million from its Services Division.

Estimated Discount To Fair Value: 25.4%

IPD Group is trading at A$4.59, below its estimated fair value of A$6.16, making it undervalued based on cash flows. Despite past shareholder dilution and recent insider selling, IPD's revenue is forecast to grow 23.6% annually—faster than the Australian market's 5.3%. Earnings are expected to increase significantly over the next three years, with a projected annual growth rate of 25.9%, outpacing the broader market's 13%.

The analysis detailed in our IPD Group growth report hints at robust future financial performance.

Get an in-depth perspective on IPD Group's balance sheet by reading our health report here.

Viva Energy Group

Overview: Viva Energy Group Limited operates as an energy company in Australia, Singapore, and Papua New Guinea with a market cap of A$4.84 billion.

Operations: The company's revenue segments include Convenience & Mobility (A$10.10 billion), Commercial & Industrial (A$16.64 billion), and Energy & Infrastructure (A$7.32 billion).

Estimated Discount To Fair Value: 20.8%

Viva Energy Group, trading at A$3.05, is undervalued based on cash flows with an estimated fair value of A$3.85. Despite past shareholder dilution and a dividend not well covered by earnings or free cash flows, VEA's earnings are forecast to grow significantly at 31.99% annually over the next three years, outpacing the Australian market's 13%. Recently added to the S&P/ASX 100 Index, analysts agree on a potential stock price rise of 25.6%.

Make It Happen

Investigate our full lineup of 37 Undervalued ASX Stocks Based On Cash Flows right here.

Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Looking For Alternative Opportunities?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include ASX:360 ASX:IPG and ASX:VEA.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]