3 Indian Growth Companies With High Insider Ownership And At Least 13% Revenue Growth

The Indian market has shown robust performance, appreciating by 1.2% over the past week and an impressive 45% over the last 12 months, with earnings projected to grow by 16% annually. In such a thriving environment, growth companies with high insider ownership can be particularly appealing as they often indicate strong confidence from those who know the company best.

Top 10 Growth Companies With High Insider Ownership In India

Name | Insider Ownership | Earnings Growth |

Archean Chemical Industries (NSEI:ACI) | 22.9% | 28.9% |

Pitti Engineering (BSE:513519) | 30.3% | 28.0% |

Kirloskar Pneumatic (BSE:505283) | 30.6% | 29.8% |

Shivalik Bimetal Controls (BSE:513097) | 19.5% | 28.7% |

Jupiter Wagons (NSEI:JWL) | 10.8% | 27.2% |

Rajratan Global Wire (BSE:517522) | 19.8% | 33.5% |

Dixon Technologies (India) (NSEI:DIXON) | 24.9% | 34.5% |

Paisalo Digital (BSE:532900) | 16.3% | 23.8% |

JNK India (NSEI:JNKINDIA) | 23.8% | 31.8% |

Aether Industries (NSEI:AETHER) | 31.1% | 40.9% |

Here's a peek at a few of the choices from the screener.

Chalet Hotels

Simply Wall St Growth Rating: ★★★★★☆

Overview: Chalet Hotels Limited is an Indian company that specializes in owning, developing, managing, and operating hotels and resorts, with a market capitalization of approximately ?170.26 billion.

Operations: The company generates revenue primarily through its hospitality segment, which brought in ?12.93 billion, and its rental/annuity business, which contributed ?1.24 billion.

Insider Ownership: 13.1%

Revenue Growth Forecast: 20.1% p.a.

Chalet Hotels has shown robust financial performance with a significant increase in quarterly and annual earnings, highlighting strong growth potential. Despite challenges such as regulatory demands from the GST department, the company's operations remain unaffected. Recent strategic appointments and management changes indicate a focus on strengthening leadership. However, it faces issues like inadequate coverage of interest payments by earnings. With high insider ownership but limited recent buying, its commitment to growth is evident though mixed with some operational concerns.

Persistent Systems

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Persistent Systems Limited is a global company engaged in providing software products, services, and technology solutions, with a market capitalization of approximately ?70.81 billion.

Operations: The revenue segments for the company are primarily divided into Healthcare & Life Sciences (?20.88 billion), Software, Hi-Tech and Emerging Industries (?45.95 billion), and Banking, Financial Services and Insurance (BFSI) at ?31.39 billion.

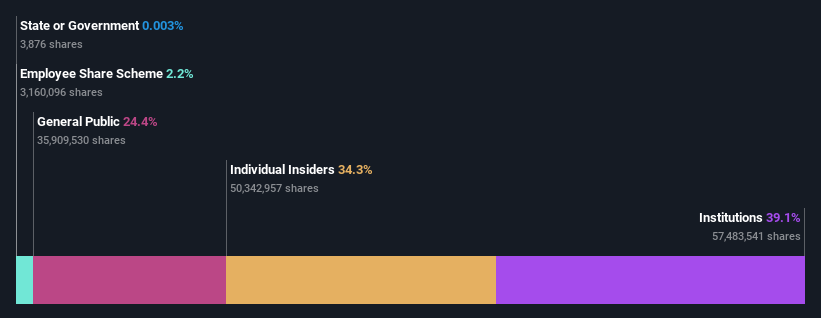

Insider Ownership: 34.3%

Revenue Growth Forecast: 13.5% p.a.

Persistent Systems, a growth-oriented firm with substantial insider ownership, has demonstrated consistent financial performance with earnings and revenue growth outpacing the broader Indian market. Forecasted annual earnings growth of 18.1% and revenue increase at 13.5% per year highlight its robust potential despite not reaching the high growth benchmark of 20%. Recent executive changes and dividend adjustments reflect ongoing corporate governance dynamics, ensuring alignment with strategic goals amidst evolving leadership roles.

Syrma SGS Technology

Simply Wall St Growth Rating: ★★★★★☆

Overview: Syrma SGS Technology Limited operates as a provider of turnkey electronic manufacturing services across India, the United States, Germany, and other international markets, with a market capitalization of approximately ?85.15 billion.

Operations: The company generates ?31.54 billion from its electronic manufacturing services.

Insider Ownership: 27.8%

Revenue Growth Forecast: 22.3% p.a.

Syrma SGS Technology, despite a dip in net income and earnings per share in the latest fiscal year, reported substantial revenue growth from INR 20.48 billion to INR 32.12 billion. This performance indicates robust sales expansion, although profit margins have compressed from previous levels. The company's revenue is expected to grow at 22.3% annually, outpacing the Indian market forecast of 9.6%. However, its return on equity is projected to remain low at 14.8%, and the recent dividend proposal appears weakly supported by free cash flows.

Where To Now?

Get an in-depth perspective on all 83 Fast Growing Indian Companies With High Insider Ownership by using our screener here.

Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Curious About Other Options?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include NSEI:CHALET NSEI:PERSISTENT and NSEI:SYRMA.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]