Discover August 2024's Undervalued Small Caps In United States With Insider Buying

In the last week, the market has been flat, but it is up 25% over the past year with earnings expected to grow by 15% per annum over the next few years. In this environment, identifying undervalued small-cap stocks with insider buying can offer unique opportunities for investors looking to capitalize on potential growth.

Top 10 Undervalued Small Caps With Insider Buying In The United States

Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

Ramaco Resources | 11.5x | 0.9x | 38.88% | ★★★★★★ |

Columbus McKinnon | 21.3x | 1.0x | 41.78% | ★★★★★★ |

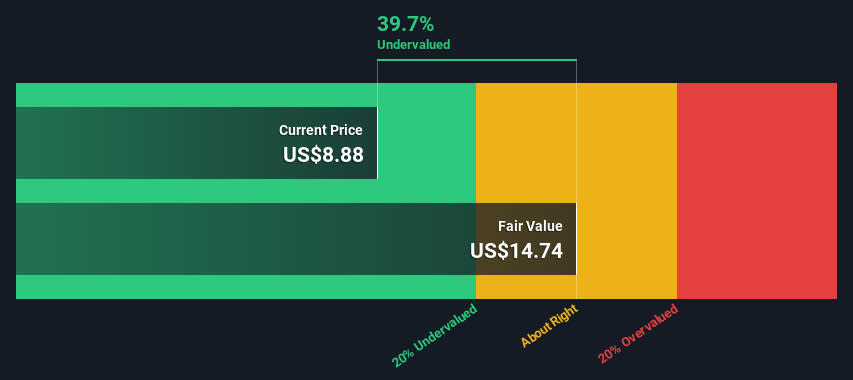

Hanover Bancorp | 8.9x | 2.0x | 49.66% | ★★★★★☆ |

Orion Group Holdings | NA | 0.4x | 18.93% | ★★★★★☆ |

Thryv Holdings | NA | 0.8x | 22.22% | ★★★★★☆ |

Franklin Financial Services | 9.7x | 1.9x | 38.50% | ★★★★☆☆ |

Lindblad Expeditions Holdings | NA | 1.0x | 35.16% | ★★★★☆☆ |

MYR Group | 34.7x | 0.5x | 41.19% | ★★★☆☆☆ |

Community West Bancshares | 18.7x | 2.9x | 42.25% | ★★★☆☆☆ |

Industrial Logistics Properties Trust | NA | 0.8x | -272.12% | ★★★☆☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

Lindblad Expeditions Holdings

Simply Wall St Value Rating: ★★★★☆☆

Overview: Lindblad Expeditions Holdings operates expedition cruises and adventure travel experiences, with a market cap of approximately $0.51 billion.

Operations: Lindblad generates revenue primarily through its Lindblad and Land Experiences segments, with recent revenues of $405.86 million and $185.61 million, respectively. The company's gross profit margin has shown a notable trend, reaching 44.10% as of the latest period ending August 26, 2024.

PE: -10.3x

Lindblad Expeditions Holdings, a small company in the expedition travel industry, recently reported second-quarter sales of US$136.5 million, up from US$124.8 million last year. Despite a net loss of US$24.67 million for the quarter, insider confidence is evident with recent share purchases by executives in August 2024. The company added two new Galápagos vessels to its fleet and appointed two experienced directors to its board, enhancing its leadership team and growth prospects.

American Woodmark

Simply Wall St Value Rating: ★★★★☆☆

Overview: American Woodmark manufactures and distributes kitchen, bath, and home organization products with a market cap of $0.71 billion.

Operations: The company generated $1.85 billion in revenue, with a gross profit margin of 20.45%. Net income margin was 6.29%, reflecting its profitability after accounting for costs and expenses.

PE: 13.4x

American Woodmark's recent earnings call on August 27, 2024, highlighted a positive trajectory despite relying solely on external borrowing for funding. The company has shown insider confidence with significant share purchases by executives over the past six months. This activity suggests strong belief in future growth potential. Their Annual General Meeting held on June 27, 2024, further reinforced this optimism among stakeholders. With its current valuation and insider activity, American Woodmark presents an intriguing opportunity within its industry.

Navigate through the intricacies of American Woodmark with our comprehensive valuation report here.

Examine American Woodmark's past performance report to understand how it has performed in the past.

Leggett & Platt

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Leggett & Platt is a diversified manufacturer that designs and produces engineered components and products found in many homes, offices, and vehicles with a market cap of approximately $4.66 billion.

Operations: Bedding Products, Specialized Products, and Furniture, Flooring & Textile Products contribute to the company's revenue streams. For the period ending 2024-06-30, gross profit was $790.80 million with a gross profit margin of 17.51%. The net income margin has shown a decline to -18.05% by this period due to significant non-operating expenses reaching $1.09 billion.

PE: -2.1x

Leggett & Platt, a smaller player in the market, has seen insider confidence with recent share purchases. Despite reporting a non-cash goodwill impairment charge of US$675.3 million for Q2 2024 and a net loss of US$602.2 million, earnings are forecast to grow at 67% annually. The company declared a dividend of US$0.05 per share for Q3 2024 and completed significant buybacks totaling US$53.27 million since February 2022, reflecting potential future value despite current challenges.

Seize The Opportunity

Reveal the 69 hidden gems among our Undervalued US Small Caps With Insider Buying screener with a single click here.

Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Ready For A Different Approach?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include NasdaqCM:LIND NasdaqGS:AMWD and NYSE:LEG.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]