Click here for Yahoo Finance’s complete coverage of the 2016 presidential election.

The wait is over: the 2016 US presidential election is here.

On Tuesday, Americans will head to the polls to cast their votes for the 45th president of the United States.

Investors, traders and analysts will closely monitor how the markets move as the votes come in. The US stock markets are likely to be closed when the final votes are tallied. But currency markets, Asian stock markets, and US futures are sure to be trading actively.

Economic data and corporate news slows down this week after a busy five days that saw the release of a Federal Reserve policy statement and a crucial jobs report.

Anxious markets, wages rising

Stocks fell again on Friday, extending a losing streak for the S&P 500 that has now gone on for nine days. The last time we saw a 9-day losing streak was back in 1980.

During this recent decline, however, the index fell just over 3%, indicating markets weren’t so much selling off as lacking direction ahead of the election.

Looking beyond the recent equity move, currency markets, notably the Mexican peso, are bracing for a big move on election night. The peso’s fortunes have risen and fallen along with those of Democratic nominee Hillary Clinton, as a Clinton presidency is seen as positive for the peso while a victory for Republican nominee Donald Trump would be negative.

Of course looming beyond any big moves in the peso is the possibility not only of a Trump win, but an unclear result on election night.

In a note this week, Capital Economics outlined a scenario in which Trump challenged a close Clinton victory, dragging markets into a prolonged period of uncertainty similar, perhaps, to what we saw following the 2000 Bush-Gore election.

With the election looming, last week featured a major run of US economic data with the latest Federal Reserve announcement crossing on Wednesday while the October jobs report came out Friday.

The Federal Reserve on Wednesday laid the groundwork for another interest rate hike, saying that, “The Committee judges that the case for an increase in the federal funds rate has continued to strengthen but decided, for the time being, to wait for some further evidence of continued progress toward its objectives.”

Economists hung on to this “further evidence” phrasing and the positive wage data we got Friday served, in the minds of many, as enough, well, evidence.

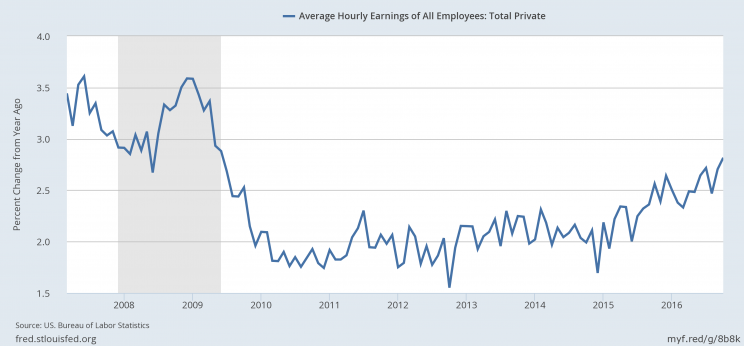

Average hourly earnings rose 2.8% over the prior year in October, the fastest clip since the recession.

Wage growth, which has been lacking despite top-line payroll gains over the last couple years, is viewed as a precursor to higher inflation. Inflation has been consistently running below the Fed’s 2% target when tracked by the central bank’s preferred measure, Core PCE.

Notwithstanding a surprise result — and a surprise market reaction — in the election this week, a December rate hike from the Fed is all but a done deal.

“In our view, the Federal Reserve can, and will likely, move policy rates at its December meeting, barring some unexpected shock to the economy or markets stemming from the election,” said BlackRock’s Rick Rieder.

“While the Fed held off from moving policy rates at its recent November meeting, we think that mostly represented a sensible hesitancy to do so a week before this highly contested general election. The fact is, as today’s payroll report continued to underscore, our economy is running very close to fully employment, and now with wages firming and likely set to rise higher, inflation should also tick up further.”

Elsewhere in the jobs report headline payroll gains totaled 161,000, a bit less than expected, while the unemployment rate fell to 4.9%.

Market Comment: Time to buy?

Despite the modest nature of the recent decline stocks, the losing streak is sure to cause some consternation among those in the market.

“That alone, no doubt, must terrify most investors and given the tightening of the US Presidential race (and Senate as well), investor anxiety has naturally been surging,” FundStrat’s Tom Lee acknowledged on Friday.

“Unfortunately, elevated investor angst is unlikely to magically evaporate completely after November 8, 2016,” BMO’s Brian Belski said.

But Belski reassured longer-term thinking investors: “While this malaise is unfortunate, this too shall pass.”

Some strategists have gotten increasingly bullish, recommending clients to take advantage of the recent pullback.

“We think election risk is now better priced, which improves reward/risk,” Deutsche Bank’s David Bianco said. “The Fed was relatively clear about hiking in December, leaving less room for a market surprise as futures now put a 75% chance on December. 3Q S&P EPS is better than expected.”

Bianco believes the next 5%+ move in the stock market will be up.

Economic Calendar

Monday: Consumer credit ($17.75 billion expected; $25.87 billion previously)

Tuesday: Job openings and labor turnover survey (5.49 million; 5.44 million previously), US presidential election (Hillary Clinton expected; Barack Obama previously)

Wednesday: No major economic reports.

Thursday: Initial jobless claims (260,000 expected; 265,000 previously)

Friday: University of Michigan consumer confidence (87.7 expected; 87.2 previously)

Click here for Yahoo Finance’s complete coverage of the 2016 presidential election.