Exploring Undervalued Small Caps With Insider Actions In Hong Kong June 2024

As of June 2024, the Hong Kong market is showing resilience with the Hang Seng Index posting a modest gain amidst mixed economic signals from mainland China. This context of fluctuating industrial outputs and retail sales growth provides a nuanced backdrop for investors looking at potential opportunities in undervalued small-cap stocks. In such an environment, identifying small-cap stocks that are potentially undervalued requires a keen understanding of market dynamics and insider actions, which can often provide critical insights into a company's future prospects.

Top 10 Undervalued Small Caps With Insider Buying In Hong Kong

Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

Wasion Holdings | 11.5x | 0.8x | 29.09% | ★★★★★☆ |

Xtep International Holdings | 10.9x | 0.8x | 42.02% | ★★★★★☆ |

Far East Consortium International | NA | 0.3x | 38.38% | ★★★★★☆ |

Sany Heavy Equipment International Holdings | 8.0x | 0.7x | -22.26% | ★★★★☆☆ |

Nissin Foods | 14.9x | 1.3x | 36.60% | ★★★★☆☆ |

China Leon Inspection Holding | 10.2x | 0.7x | 24.74% | ★★★★☆☆ |

China Lesso Group Holdings | 4.1x | 0.3x | 7.53% | ★★★★☆☆ |

Transport International Holdings | 11.0x | 0.6x | 45.45% | ★★★★☆☆ |

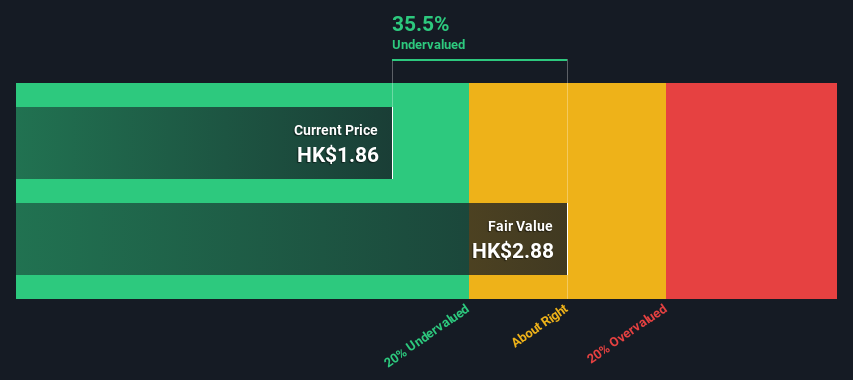

Giordano International | 8.7x | 0.8x | 35.50% | ★★★☆☆☆ |

China Overseas Grand Oceans Group | 3.1x | 0.1x | -11.60% | ★★★☆☆☆ |

Here's a peek at a few of the choices from the screener.

Abbisko Cayman

Simply Wall St Value Rating: ★★★★☆☆

Overview: Abbisko Cayman is a company focused on the development of innovative medicines, with a market capitalization of CN¥19.06 million.

Operations: The company consistently reported a gross profit margin of 100% across multiple periods, with its latest revenue recorded at CN¥19.06 million. Significant operating expenses, including R&D which recently amounted to CN¥433.74 million, have led to a net income margin improvement from -25.32% to -22.64%.

PE: -4.5x

Abbisko Cayman, a Hong Kong-based entity, recently initiated a share repurchase on June 18, 2024, signaling insider confidence by authorizing up to 10% of its issued capital for buyback. Despite lacking significant revenue (CN¥19M) and profitability forecasts for the next three years, the company is anticipated to see a substantial revenue growth of about 39% annually. This financial maneuver coupled with strategic executive changes and regulatory advancements in its pharmaceutical developments underscore a proactive approach in enhancing shareholder value amidst its current undervaluation in the market.

Click to explore a detailed breakdown of our findings in Abbisko Cayman's valuation report.

Assess Abbisko Cayman's past performance with our detailed historical performance reports.

Far East Consortium International

Simply Wall St Value Rating: ★★★★★☆

Overview: Far East Consortium International is a diversified company engaged in property development and investment across various regions including Hong Kong, Australia, and the UK, as well as hotel operations and management in multiple countries.

Operations: The company's gross profit margin has fluctuated over recent periods, with a notable increase to 0.51% in the first quarter of 2018, before a slight decrease to 0.47% by the end of that year. Revenue peaked at HK$9.61 billion in the third quarter of 2023, though this period also saw a net income margin decline to -0.017%, reflecting challenges despite higher revenue streams.

PE: -17.6x

Recently, insiders at Far East Consortium International demonstrated their confidence through significant share purchases, signaling potential undervalued status. With earnings forecasted to surge by 137% annually, this reflects a strong growth trajectory for the company. Despite relying entirely on external borrowing—posing higher financial risks—the firm remains attractive due to its dynamic market positioning and insider investment activities. These elements suggest that Far East Consortium International might be poised for future value realization.

Giordano International

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Giordano International is a global apparel retailer, operating across regions including Southeast Asia, Australia, the Gulf Cooperation Council, Mainland China, Hong Kong, Macau, and Taiwan.

Operations: In recent periods, the company has seen a gross profit margin of approximately 58.4% to 58.3%, reflecting the costs and revenues associated with its operations across various regions including Taiwan, Mainland China, Hong Kong and Macau, the Gulf Cooperation Council, Southeast Asia and Australia, as well as wholesale to overseas franchisees. The net income margin has shown variability but was reported at about 8.9% in the latest period.

PE: 8.7x

Recently, Giordano International showcased a subtle yet promising financial landscape, with first-quarter revenue slightly dipping to HK$961 million from HK$972 million year-over-year. Despite this, insider confidence is evident as they recently purchased shares, signaling belief in the company's prospects. This action aligns with their strategic executive reshuffles aiming to rejuvenate leadership and steer future growth. Amid these changes, the firm’s ability to maintain stable earnings growth at 6.37% per year reflects a resilient operational stance in a competitive market.

Make It Happen

Unlock more gems! Our Undervalued Small Caps With Insider Buying screener has unearthed 17 more companies for you to explore.Click here to unveil our expertly curated list of 20 Undervalued Small Caps With Insider Buying.

Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Looking For Alternative Opportunities?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include SEHK:2256 SEHK:35 and SEHK:709.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]