Restaurant Brands International Is Undervalued Following Recent Pullback

Shares of Restaurant Brands International Inc. (NYSE:QSR) have been in a slump lately. The stock has delivered a total return of roughly -8% thus far in 2024. Comparably, the S&P 500 has delivered a total return of around 17% over the same period. The company's shares have trailed the broader market due to a variety of factors, including multiple contraction, modestly disappointing second-quarter results and concerns that GLP-1 drugs may result in lower-than-expected long-term earnings growth potential.

The stock currently trades roughly 21 times 2024 consensus earnings per share and has a dividend yield of over 3%. While this valuation multiple is roughly in line with the broader market, it represents a significant valuation multiple discount to peers such as McDonald's (NYSE:MCD) and Yum Brands (NYSE:YUM).

Given that Restaurant Brands is a high-quality, recession-resilient business with strong growth prospects, I believe the stock deserves to trade at a premium to the broader market and is thus undervalued at current levels.

Overview

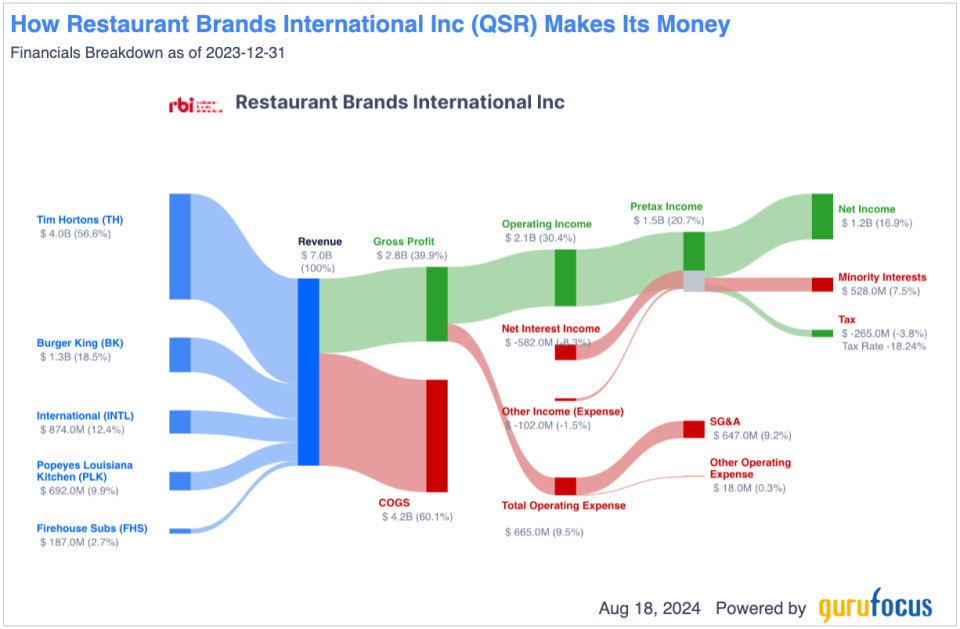

Restaurant Brands International is a leading operator of quick-service restaurant companies with a total restaurant count of more than 31,000 across more than 120 countries and territories. The company's brands include Burger King, Tim Hortons, Popeyes and Firehouse Subs. Roughly 95% of the company's restaurant locations are franchised, while the remaining 5% are company operated. Approximately 47% of its system locations are outside the U.S. and Canada.

The company generates revenue primarily through royalty and franchise fees, supply chain sales to franchisees, rental income on company-owned properties and advertising revenue fund contributions by franchisees to fund system-wide advertising costs.

The company's Tim Hortons chain is the largest contributor to operating income, accounting for roughly 41% of adjusted operating income. As a result of its capital-light business model, Restaurant Brands International has been able to generate solid net profit margins of roughly 17% despite operating in a highly competitive industry.

Ackman's Pershing Square is a key shareholder

Bill Ackman (Trades, Portfolio)'s Pershing Square is one of Restaurant Brands' largest shareholders with a roughly 23.10 million-share position worth roughly $1.6 billion at current prices. In total, the firm's holding represents roughly 7.30% of the company's total basic shares outstanding.

The guru commented on Restaurant Brands International in his 2024 mid-year shareholder letter:

In light of weakening economic conditions and ongoing boycotts, the company lowered its net restaurant and system-wide sales growth outlook this year. In response, the company is enacting a cost savings program which will enable it to grow operating profits by more than 8%. While an uncertain environment may impact unit growth in the near-term, we believe each of the company's brands will benefit in a slower economic environment with consumers trading down Despite strong performance at its largest brands, consistent operating profit growth, and a business model that benefits in a recessionary environment, QSR still trades at a meaningful discount to its peers. As the company returns to its historic mid-single-digit unit growth and delivers consistent performance at each of its brands, we believe the company's share price will more accurately reflect its improving fundamentals.

While Ackman recently trimmed the position by nearly 206,000 shares, Restaurant Brands International remains one of Pershing Square's largest holdings, accounting for approximately 16% of its total equity portfolio.

It is difficult to say for sure why Ackman decided to reduce the stake, but a few potential reasons include a desire to increase portfolio diversification, a need to raise cash to meet investor redemptions or a view that other investment opportunities are more attractive right now.

While the activist investor recently shelved plans to launch a U.S.-listed closed-end fund, he remains interested in launching a new, larger investment vehicle. For this reason, I believe Ackman may be looking to move toward a lower-risk and more diversified portfolio to protect his track record during the fundraising process.

In addition to reducing his stake in Restaurant Brands, Ackman recently decreased his position in Chipotle Mexican Grill (NYSE:CMG) and established new positions in Nike (NYSE:NKE) and Brookfield Corp. (NYSE:BN).

Given the relatively small size of Ackman's recent sales and potential motivations to build a more diversified portfolio, I do not believe the transaction should be viewed as a cause of concern for shareholders as the company's fundamentals remain strong and the valuation is attractive.

Long-term growth potential

Despite having a restaurant network with more than 31,000 locations, Restaurant Brands International remains a growth story. The company expects to deliver average annual same-store growth of 3% between 2024 and 2028. The company also expects to deliver average annual unit growth of 5% over the same period. Overall, it expects to deliver system-wide average annual growth rates and average annual adjusted operating income growth of 8% through 2028.

I view these growth targets as easily achievable as the market penetration of the company's restaurant chains remain fairly low relative to comparable peers. Burger King, which is Restaurant Brands' largest chain by store count, currently has approximately 19,500 locations globally while McDonalds has over 42,000 locations globally. Tim Hortons currently has roughly 5,800 locations globally, while Starbucks (NASDAQ:SBUX) has more than 39,000 locations. Thus, I believe the company has significant growth opportunities in terms of opening new locations. Additionally, the company is poised to deliver renewed growth at Burger King locations as it continues to focus on capital improvements to enhance existing locations as part of its reclaim the flame initiative. In April, the company announced an additional $300 million investment with franchisees to upgrade locations.

Currently, consensus estimates call for the company to report earnings per share growth of 13.90% in 2025, 10.40% in 2026 and 15% in 2027. Thus, Wall Street analysts are currently fairly confident that the company will be able to deliver on its growth plans. I agree with this view and expect it to deliver double-digit earnings growth over the next few years. One of the reasons why I am especially bullish on the company's growth prospects is that from a profitability standpoint, Tim Hortons is the company's most attractive brand as it accounts for roughly 43% of operating income (excluding locations outside the U.S. and Canada, which are part of the international segment), while the much larger Burger King chain accounts for just 18% of operating income (excluding locations outside the U.S. and Canada, which are part of the international segment.) Tim Hortons is the company's most profitable segment as it is the primary supplier of products and supplies as well as consumer packaged goods to the franchisees. Comparably, the company does not own the supply chain that services Burger King, Popeyes and Firehouse Subs and instead relies on third-party suppliers.

With under 6,000 locations globally, I believe Tim Hortons has greater location growth potential compared to the larger Burger King chain. Moreover, Tim Hortons is performing quite well with reported same-store sales growth of 4.60% on a year-over-year basis during the second quarter, while the Burger King chain experienced a decline of 0.10% over the same period.

Attractive valuation and dividend yield

Restaurant Brands International's forward price-earnings multiple of 21, based on full-year 2024 consensus estimates, is somewhat lower than peers and slightly lower than the broader market, which trades at around 22 times forward earnings. Given the relatively low cost of dining out at fast-food restaurants, these companies tend to trade at a premium to the broader market as their earnings are less cyclical. McDonald's trades at a forward price-earnings ratio of 23.50, while Yum Brands trades at a forward earnings multiple of 24.

Yum Brands is expected to grow annual earnings per share by 11.50% in 2025 and 2026 and 14.40% in 2027, while McDonald's is expected to grow earnings per share by 7.90%, 8.20% and 12.60% over the same periods. Comparing these projections with the ones for Restaurant Brands, on a relative basis I do not believe the company's valuation discount is warranted relative to peers. Moreover, given the fact the company has a fairly recession-resilient business and near-term earnings growth expectations, which are in line with the broader market, there is a solid case to be made that the stock should trade at a modest premium.

In addition to trading at an attractive valuation relative to peers, Restaurant Brands International also offers a higher yield. Currently, the company has a dividend yield of around 3.30%, while McDonald's and Yum Brands have dividend yields of 2.40% and 1.90%.

In terms of valuation relative to its own historical norms, Restaurant Brands also appears to be undervalued as the stock has traded at a median price- earnings ratio of roughly 26 over the past 10 years.

GLP-1 drugs remain a potential risk to the bull case

GLP-1 drugs pose a threat to Restaurant Brands as they have the potential to result in decreased consumption of unhealthy foods such as burgers and fries, which make up a key part of its business. Some studies have suggested GLP-1s have led consumers to cut back on dining out in general. While it is too early to estimate the full impact these drugs will have on the company's business, I think it is fair to say the impact has been modest thus far as it reported system-wide same-store sales growth of 1.90% in the most recent quarter. While this level of growth is lower than the previous year's growth rate of 4%, it is still positive despite massive adoption of the weight loss drugs over the past year.

Conclusion

Restaurant Brands International represents a high-quality business with solid growth prospects. The stock is currently trading at a discount to the broader market, peers and its own historical median valuation. I believe the company is likely to deliver on its ambitious growth plans in the coming years and that earnings per share are likely to grow by double-digit annual rates over the next few years. Moreover, the stock offers a solid dividend yield and some resilience to an economic slowdown. For these reasons, I view the stock as undervalued at current levels and an attractive investment.

This article first appeared on GuruFocus.