Here Are My Top 5 Dividend Stocks to Buy in August

After a spectacular performance in 2023 and a roaring start to 2024, the capital markets have started to cool down as of late.

Naturally, the recent selling activity can be attributed to a variety of factors including mixed job data, the Federal Reserve's monetary policy outlook, and of course the upcoming presidential election. During times like these investors may opt to exit more growth-oriented opportunities and seek safer, steadier positions.

Let's explore five dividend stocks that I think look like screaming buys right now. Investors interested in reliable passive income don't want to miss out on these stocks.

1. Hercules Capital

Hercules Capital (NYSE: HTGC) is a business development company (BDC) that specializes in high-yield loans to venture-backed companies. BDCs are required to pay out at least 90% of their taxable income each year in the form of a dividend, hence they can be lucrative sources of passive income.

Generally speaking, a bank may avoid making a loan to a young company. And if it does, it likely won't be a material enough amount to provide adequate runway.

Hercules differentiates itself from banks due to the way it structures deals. For example, while a bank may have a dollar threshold, Hercules generally offers larger term loan sizes but at a higher interest rate. Moreover, Hercules also generally attaches warrants to its deals, which act as a sweetener if a portfolio company ends up getting acquired or goes public.

A good measure of a BDC's health is to look at its non-accrual investments. Essentially, these are investments that the company sees as highly unlikely to pay back principal and interest.

For the quarter ended June 30, only 2.5% of Hercules' $3.6 billion portfolio was categorized as non-accrual status.

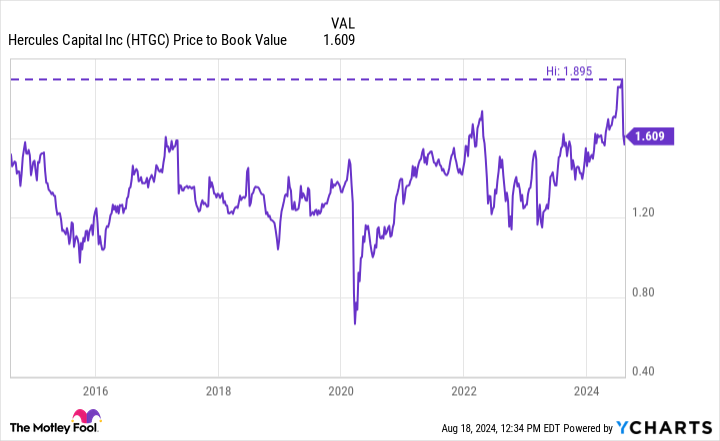

Right now, Hercules trades at a price-to-book (P/B) ratio of 1.6, which is close to its highest level in 10 years. Its total return over the last decade is 229%, handily outperforming the S&P 500's total return of 184%. So even though Hercules stock isn't exactly cheap, I think the premium is well deserved.

With shares trading at a 10.4% dividend yield, I think now is as good a time as ever to load up on Hercules and prepare to hold for the long run.

2. Ares Capital

Another BDC on my list is Ares Capital (NASDAQ: ARCC). Ares is quite different than Hercules, however, as the company has wider industry coverage and offers more sophisticated financial products.

Furthermore, with 50% of its total portfolio allocated toward first lien senior secured loans, investors can rest easy that Ares is well positioned even in downside scenarios.

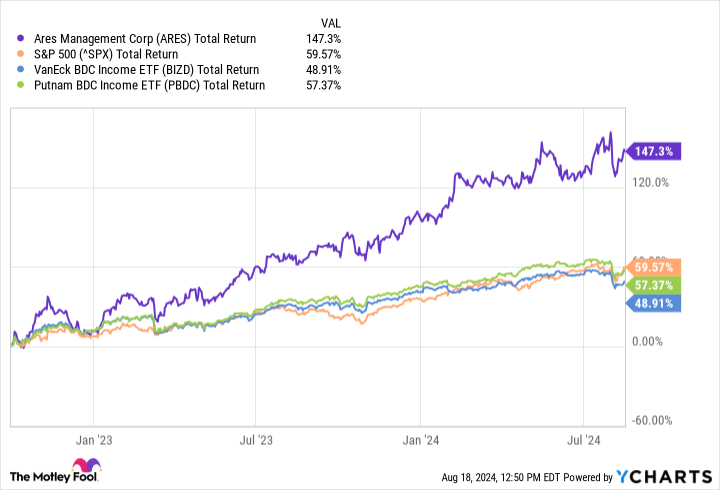

Per the chart above, investors can see that Ares has handily outperformed the S&P 500 as well as leading BDC-focused exchange-traded funds (ETFs) over the last couple of years. Considering how strong the S&P 500 has been since its massive sell-off in 2022, it's impressive just how much Ares has outperformed its peers and the broader market.

While it may not be as attractive as a high-growth AI stock, Ares has quietly been a multibagger opportunity for its shareholders. Investors may want to consider augmenting their gains with this passive income player, as shares yield around 9.3% right now.

3. AT&T

I'll admit right off the bat that telecom businesses aren't overly exciting, and AT&T (NYSE: T) is no exception. The telecom industry is pretty commoditized, which essentially forces the big players to compete on price.

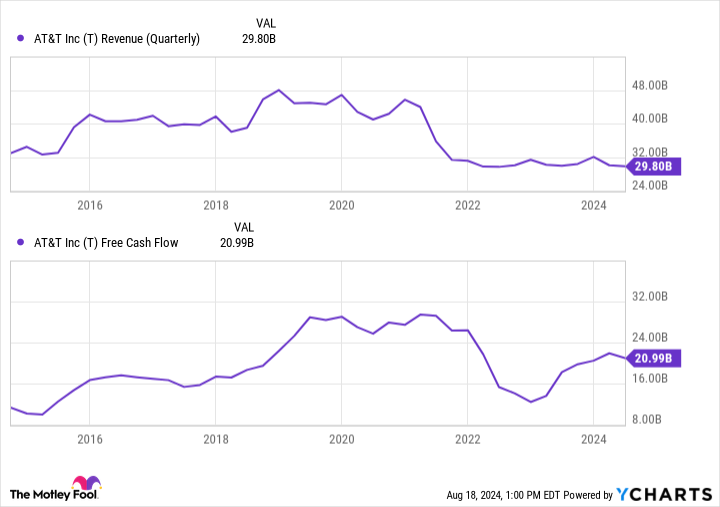

When you're in the business of offering the lowest-cost solution, it can be hard to grow. As the chart above illustrates, AT&T's revenue has dropped considerably over the last decade. Again, an overcrowded market coupled with ongoing churn dynamics plaguing the communications sector isn't exactly a recipe for hypergrowth.

Nevertheless, AT&T has demonstrated a disciplined approach to costs during this time of decelerating sales. For that reason, the company has been able to actually increase its free cash flow despite some dramatic ebbs and flows in the top line.

It is important to note that some of this cash flow was augmented by AT&T slashing its dividend nearly in half back in 2022. Although that's not overly encouraging, I'll give AT&T's management some credit.

As of the end of the second quarter, AT&T's net debt was $127 billion. This was an improvement of about $5 billion compared to the second quarter of 2023. Should AT&T remain focused on strengthening its balance sheet, I see little reason for the company to cut its dividend again.

So while AT&T isn't going to supercharge your portfolio by any means, I think the stock offers a compelling turnaround opportunity. Moreover, AT&T's current price-to-earnings (P/E) ratio of 11.1 is hovering near all-time lows. While some may have soured on AT&T for good, I think now is a good opportunity to scoop up shares at dirt cheap levels and take advantage of the 5.7% yield.

4. Verizon

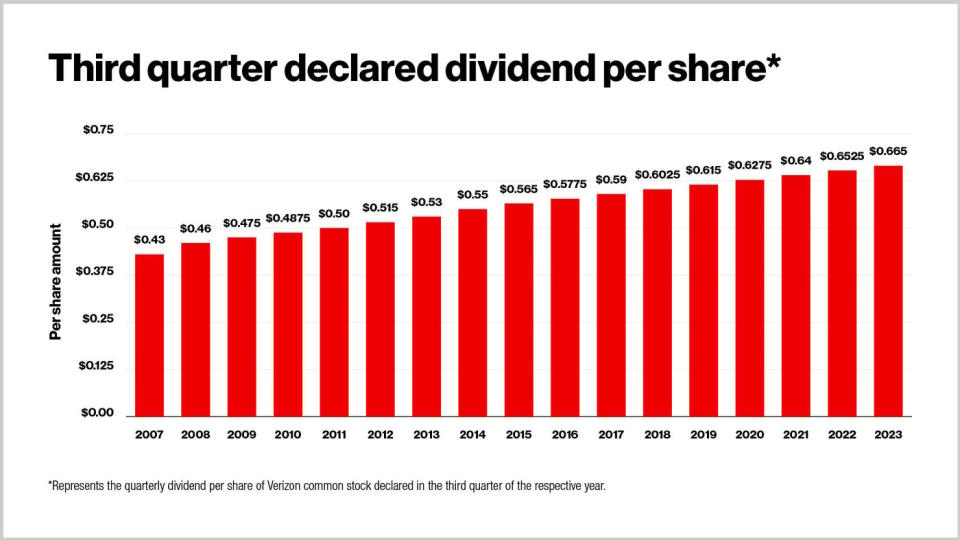

Next up on my list is one of AT&T's biggest competitors, Verizon Communications (NYSE: VZ). The bulk of my thesis for investing in Verizon is illustrated in the graphic below.

Last September marked 17 consecutive years of dividend raises for Verizon. Moreover, when speaking about commitment to subsequent dividend raises, Verizon's CEO Hans Vestberg said that he wants to "continue to put the Board in a position to do that" during the company's second-quarter earnings call.

To me, Verizon is not only a reliable dividend opportunity; I think a raise could be on the horizon next month. Such action could inspire a little jolt in the stock, so I'd be a buyer right now. Verizon's P/E of just 15.2 pales in comparison to the S&P 500's P/E of 27.5. With shares yielding about 6.5%, now looks like a terrific opportunity to invest at a steep discount to the broader market.

5. Altria

In my opinion, I've saved the best for last. Altria (NYSE: MO) is the tobacco company behind notable cigarette brands such as Marlboro and Black & Mild, and is also notably a Dividend King. The tobacco industry is no doubt experiencing an existential crisis. A larger cohort of consumers are becoming more mindful of health and wellness, making tobacco products a tough sell.

But like all great companies, Altria has found ways to navigate this challenge. Management has stated that Altria's next phase hinges on "moving beyond smoking."

Namely, the company is focusing more attention on vaping products as well as oral nicotine pouches as opposed to traditional smoking products. Although this transition is in its early stages, there are strong indications that this pivot is working.

Last June, Altria acquired vaping company NJOY. At the time, NJOY products could be found in roughly 35,000 stores nationwide. Per Altria's second-quarter earnings presentation, NJOY's footprint has almost tripled to 100,000 stores.

Although the aggressive expansion efforts might suggest NJOY is in high demand, the brand currently only owns about 5% of U.S. retail share. To me, this bodes well for NJOY's long-run momentum and validates Altria's investments and focus on smokeless tobacco.

Another reason why I love Altria stock is that the company has been actively buying back shares for some time now. Through the first six months of 2024, Altria repurchased $2.4 billion of stock at an average price of $44.50.

Companies may opt to buy back shares when management thinks the stock is undervalued. Considering Altria currently trades at about $51 per share, the company's repurchase program is looking pretty savvy right about now.

Given its consistent history of raising its dividend, coupled with an exciting new chapter featuring the next frontier of the tobacco industry, I see Altria as an outstanding opportunity for investors seeking a combination of gains and reliable passive income.

Should you invest $1,000 in Altria Group right now?

Before you buy stock in Altria Group, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Altria Group wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $787,394!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 22, 2024

Adam Spatacco has no position in any of the stocks mentioned. The Motley Fool recommends Verizon Communications. The Motley Fool has a disclosure policy.

Here Are My Top 5 Dividend Stocks to Buy in August was originally published by The Motley Fool