Business sentiment has been shaken by U.S. President Donald Trump’s escalating trade war with China, the European Union and other countries, financial analysts say. But some are wondering why the impact hasn’t shown up in the hard economic data. And while the stock market has been volatile, it certainly could be a lot lower considering the nature of the political rhetoric.

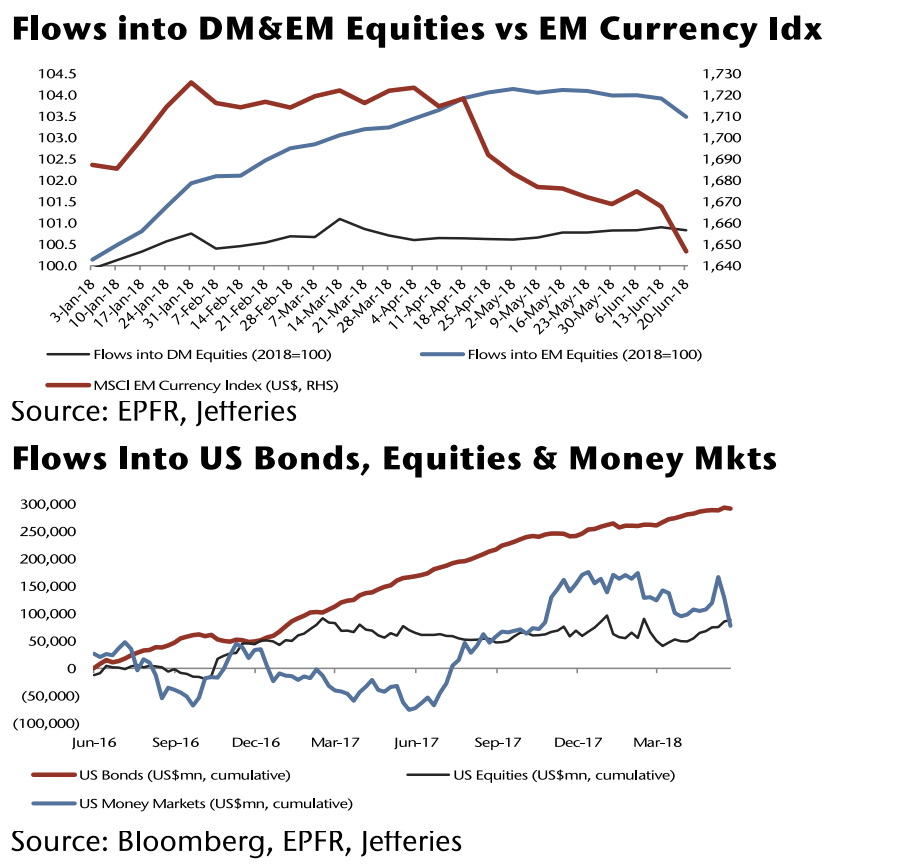

Unlike in February when Trump first began saber rattling about trade tariffs and markets swooned, investors so far in June have continued to favor U.S. assets. Traders poured $3.4 billion in net funds into U.S. equities last week, according to analysis from Jefferies and Co., marking the seventh straight week of inflows.

In contrast, fund flows in the rest of the world have been sharply negative as investors have taken refuge in American assets.

‘The least ugly duckling’

“There was a clear-cut preference toward the U.S.,” Jefferies analysts said in a note, pointing out that equity markets in Asia, Europe, the Middle East and Africa as well as Latin America had seen outflows ranging from nearly $5 billion in Asia to $506 million in Latin America, the highest level in the region since March 15.

On the currencies side, the dollar has strengthened over the past few months against rivals from both developed and emerging countries.

John Doyle, vice president of dealing and trading at Tempus Inc in Washington, argues that the United States and U.S. assets are gaining steam because there’s simply nowhere else for traders to turn in the current environment of risk avoidance.

“The U.S. and the dollar are the least ugly duckling,” Doyle said.

A couple major tailwinds

U.S. assets also have a couple substantial tailwinds pushing them higher: higher interest rates and government spending. The Federal Reserve’s rate projections show the U.S. central bank is poised to raise interest rates twice more this year and outlines three more hikes in 2019. If those projections hold true, the U.S. will boast overnight interest rates of 3.25-3.50% by the end of next year.

Higher interest rates make a currency more attractive for traders to hold. It’s also a sign of a stronger economy. The European Central Bank is holding rates in the euro zone at zero or in negative territory and the Bank of Japan also has negative rates for some deposits.

Still, because of the so-called response drag the impacts of the Fed’s hikes are not felt by consumers for up to 18 months after they are implemented, meaning the U.S. economy is still also benefitting from the stimulus of loose monetary policy.

On the fiscal side, the $1.5 trillion tax cut Trump signed in December and a congressional budget deal that increased government spending by $300 billion are also helping buoy the market.

“The federal government’s going to spend a lot of money that supports the overall economy in a way that we haven’t seen for a number of years,” Kate Warne, principal and investment strategist at asset manager Edward Jones, told Yahoo Finance earlier this year. “The chances of economic growth slowing a lot in an environment where the federal government is literally putting a lot more money to work in the economy is pretty low.”

Those tailwinds have helped unemployment fall to its lowest level since the 1970s and put U.S. gross domestic product on pace to grow up to 5% this quarter. However, the stimulus they have provided is a double-edged sword.

Will it be different this time?

The Fed is raising rates at an unprecedented time. According to Deutsche Bank, in the 118 rate hikes since 1950, nominal GDP growth has been below 4.5 percent only twice. U.S. nominal GDP growth in 2017 was about half that level.

Hiking rates into such a fragile economic backdrop could be risky and beg the question of “whether this time is different,” Deutsche analysts said.

Further, others see the potential for problems when the U.S. moves from monetary policy stimulus to fiscal stimulus, as Trump increases fiscal spending while the Fed reduces monetary stimulus by raising rates.

“We worry about the shift from massive monetary stimulus to fiscal policy picking up the baton and that’s where stuff often happens – as in somebody could drop the baton,” Cyrus Taraporevala, president and chief executive officer of State Street Global Advisors, said last month at an investment summit in Manhattan. “We definitely see more uncertainty and volatility.”

Market analysts and fund managers, including hedge fund billionaire Paul Tudor Jones, also worry that asset values are too high and that if a downturn comes there will be little room to maneuver. Interest rates are still low by historical standards and fiscal policy has largely been exhausted, Jones said.

It remains to be seen whether the trade war will have a negative impact on employment or growth, but it is already showing up in economic data, according to Deutsche Bank Chief International Economist Torsten Slok.

“It is striking that the significant tailwind from corporate tax cuts is now being offset by other forces,” he said in a note highlighting recent weakness in U.S. PMI reports, which track the health of the manufacturing sector. “Most likely the uncertainties associated with the ongoing trade war.”

See also:

The emerging markets feel-good story of the decade has imploded

Blankfein: The immigration debate isn’t as simple as right and wrong

Trump’s trade war is undercutting his hopes for the dollar

—

Dion Rabouin is a markets reporter for Yahoo Finance. Follow him on Twitter: @DionRabouin.

Follow Yahoo Finance on Facebook, Twitter, Instagram, and LinkedIn.