7 Stocks That Will Benefit the Most From Coming Rate Cuts

After a period of aggressive interest rate hikes aimed at taming inflation, the Federal Reserve is poised to shift gears in the coming months. With inflation moderating and approaching the Fed’s 2% target, economists and investors anticipate rate cuts as early as September 2024.

Lower interest rates typically benefit certain sectors through lower borrowing costs and by spurring higher demand. However, there is also another way lower rate cuts can help companies this year. COVID forced many companies to take on crushing levels of debt, and the rate hikes have made it exceedingly difficult for these companies to hold their head above water.

That said, once rates come down, these companies and their earnings will rebound.

InvestorPlace - Stock Market News, Stock Advice & Trading Tips

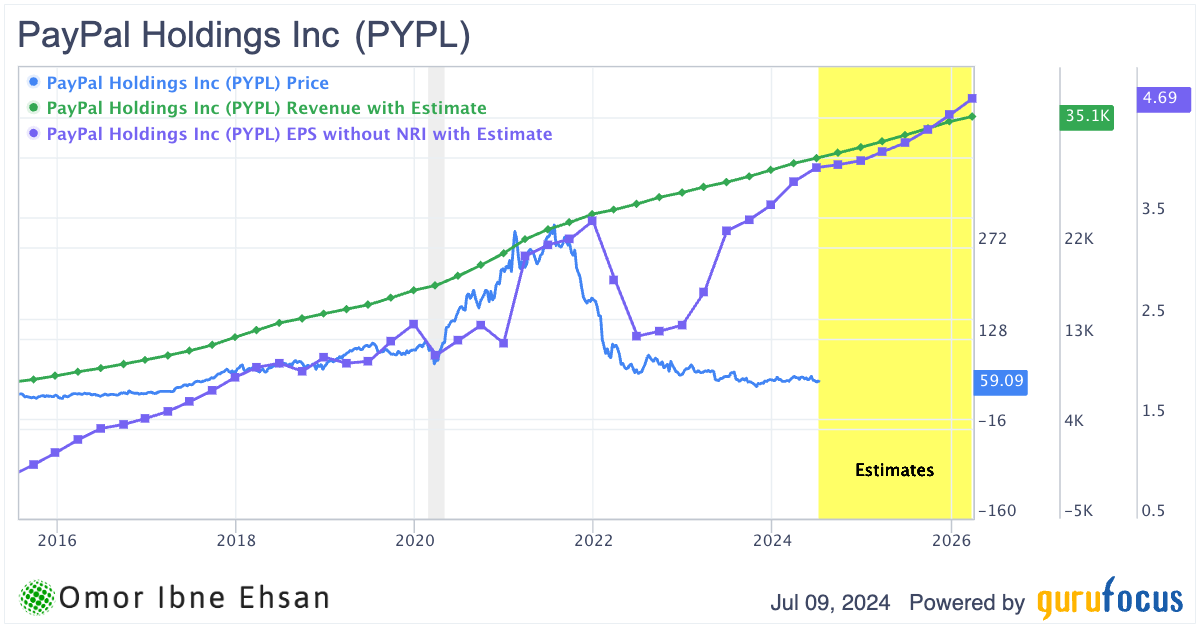

PayPal (PYPL)

Source: Tada Images / Shutterstock.com

PayPal’s (NASDAQ:PYPL) stock has been a laggard, but I’m optimistic about where the company is headed. The digital payments space continues to grow rapidly. In its Q1 earnings report, PayPal beat revenue expectations with 9% growth and saw a 14% increase in total payment volume. New CEO Alex Chriss seems to be steering the ship in the right direction.

Several analysts have recently upgraded their ratings on PayPal, with price targets as high as $90. The consensus is a moderate buy. The company’s strong brand recognition positions it well to capitalize on the shift to digital commerce.

The Fed’s potential interest rate cuts could also benefit PayPal. Lower rates tend to boost consumer spending and make borrowing cheaper for businesses looking to invest in growth, which could drive increased payment volumes for PayPal. It could also cause a rebound in account growth, which is why PayPal remains depressed despite core financials remaining resilient. If the Street paid more attention to core financials, PYPL would have made a huge recovery ages ago.

Source: Chart courtesy of GuruFocus.com

Of course, there are risks to consider. Competition in digital payments is fierce, with players like Apple Pay, Cash App and others vying for market share. To maintain its edge, PayPal will need to continue innovating and providing a seamless user experience. Overall, though, the long-term trends favor PayPal.

Six Flags Entertainment (FUN)

Source: Martina Badini/Shutterstock.com

Six Flags Entertainment (NYSE:FUN) now trades under the ticker FUN after its $8 billion merger with Cedar Fair. It is poised to become the largest amusement park operator in the U.S. This deal creates a new titan, with 42 parks across 17 states. While diehard rollercoaster fans are watching the integration closely, I believe the company has some strong tailwinds at its back.

First, interest rates are widely expected to decline over the next two years as inflation recedes. This should boost Six Flags, as its hefty $158.3 million in annual interest expense will become less of a burden on the bottom line. Lower rates could also spur more consumer spending on leisure and entertainment.

Moreover, early indications are that per capita spending at the parks continues to grow nicely, with Q1 in-park revenues hitting a record. Season pass sales are also tracking well above last year. The stars may finally be aligning for this long-struggling theme park operator.

Synchrony Financial (SYF)

Source: rafapress/Shutterstock.com

Synchrony Financial (NYSE:SYF) is making some savvy moves to position itself for growth despite near-term headwinds from the CFPB’s new late fee rules. The company is proactively raising interest rates and adding fees to offset the expected hit to late fee revenue. While not ideal for consumers, Synchrony is nimble and focused on protecting its bottom line.

Looking ahead, I see some megatrends working in Synchrony’s favor. The continued growth of e-commerce and digital payments plays to Synchrony’s strengths in private label credit cards and financing programs with hundreds of retailers and merchants. As the economy normalizes post-pandemic, Synchrony should benefit from higher consumer spending.

Even with high interest rates, Synchrony also returns cash to shareholders, recently boosting its buyback authorization by $1 billion.

The key tailwind I’m watching is the potential interest rate cuts in 2024. The Fed has signaled several quarter-point cuts could be on the table. This would help reduce Synchrony’s interest expense on its deposits and debt, boosting margins and earnings power. Lower rates could also spur more borrowing and spending by consumers.

The stock comes with a 2.1% dividend yield.

Weyerhaeuser (WY)

Source: rafapress / Shutterstock

Weyerhaeuser (NYSE:WY) is navigating the challenging market conditions quite well. In Q1, they generated solid net earnings of $114 million and grew adjusted EBITDA by 10% compared to Q4 2023. That’s impressive in this environment.

The long-term fundamentals for housing remain very favorable. There are also strong demographic trends, with a rise in smaller family units. As mortgage rates stabilize with potential Fed rate cuts on the horizon, lumber demand and pricing should be a nice boost. Lower rates would also help reduce Weyerhaeuser’s interest expense, which came in at $280 million last year. Every little bit helps!

They also progress in new growth areas like solar energy and carbon capture projects. Management is making smart moves to leverage their massive landholdings and generate new revenue streams. Recent analyst reports echo my positive sentiment—RBC Capital maintained its Outperform rating with a slightly lower $37 price target. However, today’s stock trading at around $28 implies a nearly 35% upside.

WY stock also has a 2.9% dividend yield.

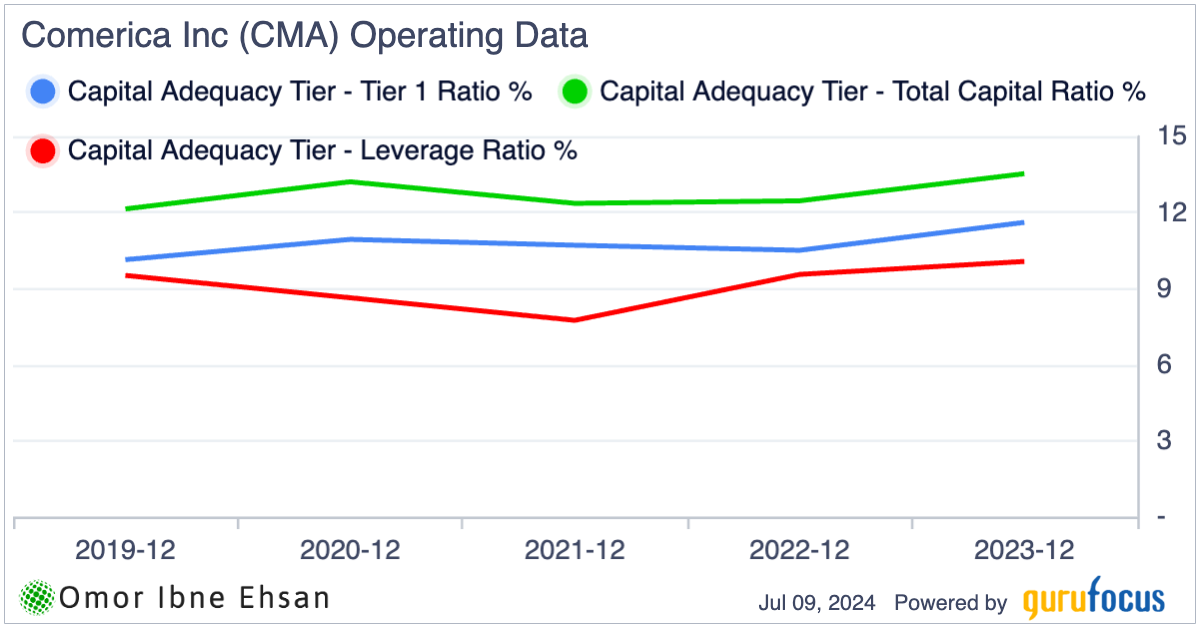

Comerica (CMA)

Source: Lester Balajadia / Shutterstock.com

Comerica’s (NYSE:CMA) stock has steadily recovered, but sunnier skies are ahead. The company recently reported solid Q1 2024 earnings, with core EPS beating estimates. Deposits held up better than expected, and credit quality remained strong despite some normalization.

Comerica is poised to benefit from the economy picking up steam in the second half of 2024. Comerica’s economists forecast a return to growth, which should boost loan demand and help Comerica’s bottom line. CAT ratios are already recovering to pre-pandemic levels.

Source: Chart courtesy of GuruFocus.com

Moreover, many expect the Fed to cut interest rates later this year. As funding costs decline, Comerica’s net interest income will be lifted. The company’s interest rate swaps and securities portfolio maturities should also act as earnings drivers in the coming quarters.

The stock also comes with a 5.67% dividend yield.

Crown Castle (CCI)

Source: Casimiro PT / Shutterstock.com

Crown Castle (NYSE:CCI) is navigating a complex set of circumstances in 2024, but I believe the company is well-positioned to capitalize on key megatrends in the years ahead. The ongoing rollout of 5G networks and society’s insatiable demand for mobile data are powerful tailwinds that should drive demand for Crown Castle’s tower, small cell and fiber infrastructure for the foreseeable future.

That said, it hasn’t been all smooth sailing lately. Activist investors are pressuring Crown Castle to sell its fiber business, and the company recently cut its workforce by 10% and lowered profit forecasts as part of a strategic review. New CEO Steven Moskowitz certainly has his work cut out for him.

But there are reasons for optimism. While Crown Castle’s total debt load has ballooned to concerning levels, over 90% is fixed-rate with an average maturity of 7 years. This provides some insulation against rising rates. And if rates get cut, it would give a nice boost by lowering the company’s interest expense, totaling $835 million in 2023. It will be a bumpy ride, but Crown Castle presents a compelling long-term opportunity for patient investors.

The dividend yield here is 6.48%.

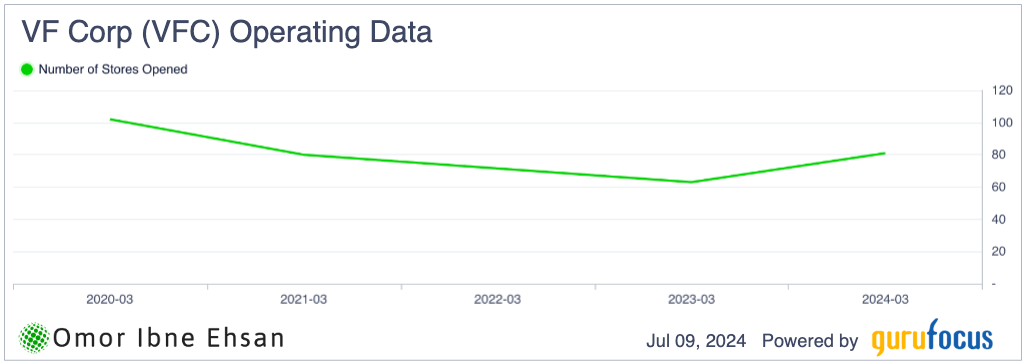

V.F. Corporation (VFC)

Source: rblfmr / Shutterstock.com

V.F. Corporation (NYSE:VFC) is experiencing a challenging period but is taking steps to turn things around. The company missed revenue and earnings estimates in Q4 2024, with revenue declining 13% year-over-year.

However, new CEO Bracken Darrell, who took over 10 months ago, is implementing a ” Reinvent ” transformation plan to reset the business. This has already led to stronger-than-expected cash flow in Q4. Key priorities are fixing the struggling Americas business, turning around the Vans brand and paying down debt. Annual store openings have now started to rebound.

Source: Chart courtesy of GuruFocus.com

Interest expense will be an important factor to watch. In fiscal 2024, VF had gross interest expense growth of 72%, likely due to its high debt load. However, the company is focused on deleveraging—it reduced net debt by $540 million in Q4 alone. Potential interest rate cuts by the Fed would provide a nice tailwind by reducing VF’s borrowing costs in the future. This stock also has a 2.68% dividend yield.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

On the date of publication, the responsible editor did not have (either directly or indirectly) any positions in the securities mentioned in this article.

Omor Ibne Ehsan is a writer at InvestorPlace. He is a self-taught investor with a focus on growth and cyclical stocks that have strong fundamentals, value, and long-term potential. He also has an interest in high-risk, high-reward investments such as cryptocurrencies and penny stocks. You can follow him on LinkedIn.

More From InvestorPlace

The post 7 Stocks That Will Benefit the Most From Coming Rate Cuts appeared first on InvestorPlace.